US Manufacturing Sector Anticipates Sharp Sales and EPS Growth Decline in 2019

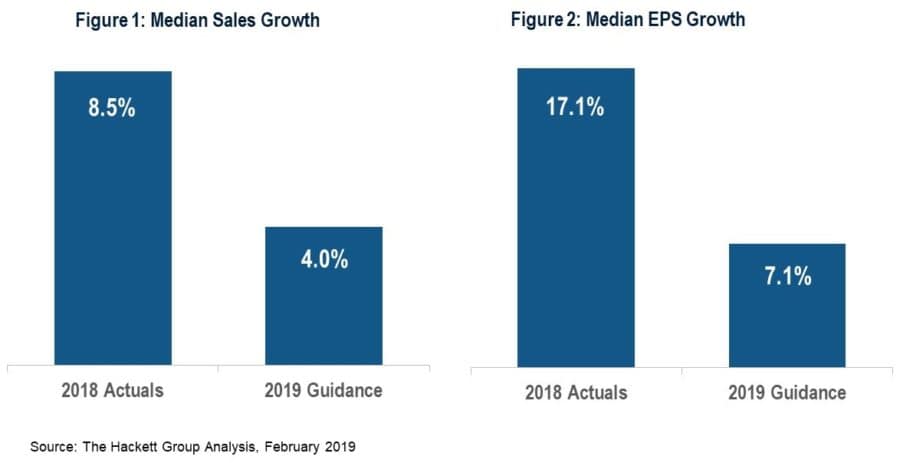

Guidance issued to date by US manufacturing companies during the Q4 2018 earnings release cycle points to a sharp decline in growth in 2019. Compared with reported actual 2018 Sales growth of 8.5%, growth of only 4.0% is projected for 2019. At the same time, EPS growth is projected to be 7.1%, down from 17.1% in 2018. This outlook has major repercussions for the manufacturing sector and will force many manufacturing companies to continue slashing costs to protect margins.

In 2018, 65% of 223 manufacturing companies included in our analysis met or exceeded 2018 Q4 earnings estimates. Further, of those companies providing Q4 EPS guidance, all but 4 (88%) met or exceeded that guidance, resulting in stellar overall earnings growth performance for American manufacturers in 2018, bolstered in part by the one-off effect of the tax cuts.

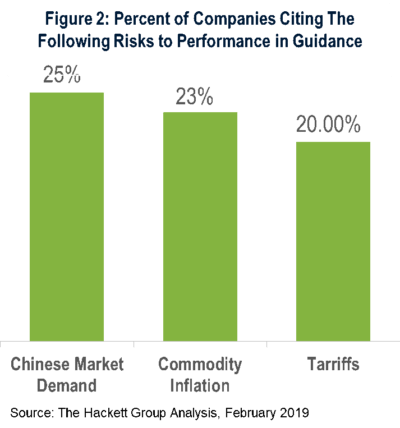

However, manufacturing companies that provided EPS and revenue growth guidance[1] are offering a much bleaker outlook for 2019. Median 2019 EPS growth guidance is 7.1%, down from historically high actual EPS growth of 17.1% in 2018 (Fig 1). Projections from companies providing guidance also indicate a sharp reduction in revenue growth in 2019 to 4.0%, down from top line growth of 8.5% in 2018. The reasons cited for these uninspired performance projections are markedly consistent, including: declining Chinese market demand; increased commodity price pressures; and the impact of tariffs.

25% of manufacturers cited a slowdown of demand in China as a 2019 earnings and growth risk. For example, in their Q4 earnings release, PPG Industries commented: “looking ahead, we expect regional sales volumes in automotive OEM and general industrial coatings to remain negative in the first quarter as industrial activity in China is anticipated to continue to be more volatile.”

Input cost inflation is a second major concern – including energy, commodities, labor and services like transportation – and is surfacing as a challenge for 2019, cited by 23% of companies as weighing on performance guidance for 2019.

Finally, tariff concerns are a major influence on earnings outlook, cited by 20% percent of companies, ranging from consumer companies like Whirlpool to niche technology players like Roper Industries.

“2018 was a good year for earnings in the manufacturing sector – boosted by the tax cut,” states Dave Sievers, a Principal with The Hackett Group, “but companies are not sure where the economy is headed for 2019. While there are some positive signals, volatile conditions of the Chinese market, and uncertainly about tariffs and input costs are serious risks resulting in pressure to manage and optimize costs in 2019. In the face of an expected slowdown in top line growth, it’s clear that companies will need to be even more focused on significant cost reductions to achieve bottom line guidance in 2019”

The Hackett Group recommends that companies focus on transformational cost initiatives that can be readily identified through the use of our proprietary automated tool and methodology, the digital transformation platform. This tool compares enterprise cost profiles, benchmarks performance, pinpoints cost optimization opportunities, and helps to define and implement programs to deliver sustainable improvements.

Additionally, Hackett can help manufacturing companies optimize cost though implementation of leading cloud-based application platforms such as SAP, Oracle, Ariba and Coupa.

[1] Representing 37 companies included in our analysis

Related Insights

As SG&A Pressure Mounts, a 75% AI Performance Gap Is Emerging

Finance has the clearest view of the artificial intelligence (AI) opportunity. AI World Class research shows organizations redesigning work around…

The Hackett Group® – As Seen on CNBC

Leading the way in Gen AI solutions, we are redefining what Digital World Class® performance looks like and accelerating your…

Solution Intelligence Programs

Too many providers. Too many claims. Too little evidence. Solution Intelligence gives enterprise leaders independent, data-backed insight into which solutions…

Applied Intelligence Programs for Executives

AI is accelerating decisions and increasing the cost of getting them wrong. Applied Intelligence helps leadership teams cut through complexity,…