Using DSO to Measure Receivables; Part 1 – Definition & Calculation

What is the best key performance indicator (KPI) to measure accounts receivable (AR)? Over the years there has been a lot of debate – days sales outstanding (DSO), days billing outstanding (DBO), collections effectiveness index (CEI) and accounts receivable turnover (ART) – but all have their proponents. It is important to get the best fit for your company’s structure, culture and goals. This review takes a closer look at DSO.

Part 1: Definition and calculation of DSO

DSO is often defined as “the average amount of time in days it takes to receive payment.”. This is not correct – more accurately, it reflects the value of receivables outstanding with customers, expressed in the equivalent number of days of revenue.

Opinions vary as to whether DSO should be reported on a monthly, quarterly, half yearly or annual basis. As with the KPI itself, the right reporting frequency will depend on the organisation. At the local operating company level, we recommend monthly measurement with a minimum of a 13-month trend line (or longer, if the business is highly seasonal) to closely monitor collection effectiveness. Often, it is only reported on a quarterly or half yearly basis. When this is the case, performance usually deteriorates after one reporting period – due to a lack of visibility leading to a reduced focus -, and will only improve at the next. This type of trend does not drive optimal cash flow.

DSO can be calculated in several ways. The most common method is the rolling average which smooths out seasonal variations. This calculates the ‘X’ month rolling average of sales (three months, six months or twelve months) outstanding. It is recommended mostly for corporate level reporting, for businesses that can have a lot of fluctuation in revenues and performance and are more concerned about the direction of the trend line over a defined period.

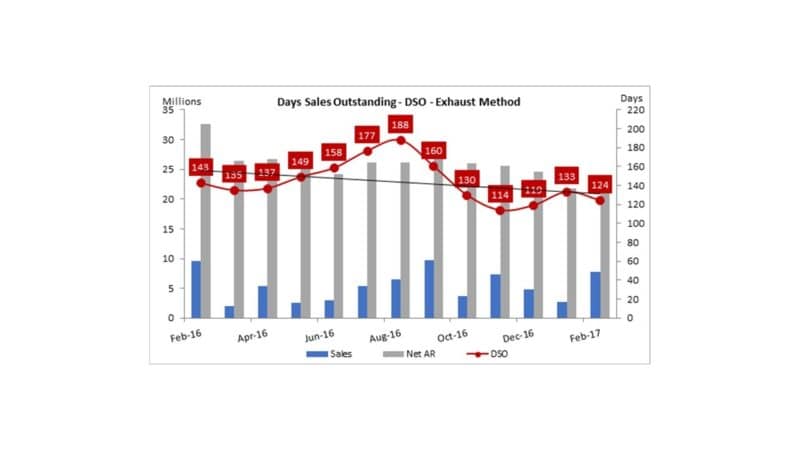

A more accurate calculation is the exhaust (or count back) method. This measurement expresses the value of AR at the end of each month, in the number of days of sales (with most weight on the most recent month) it is equivalent to. This highlights actual monthly performance, and will allow for immediate remedial action when there is deterioration.

In the graph, it is possible to see how performance can improve when AR drops and sales increase (November – 114 days). In December, the opposite happens; the DSO reflects a deterioration caused by lower sales with AR reduced but not to the same degree, reflecting higher overdues and therefore an increased DSO.

Related Insights

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Summary Report

Artificial intelligence (AI) capabilities are advancing faster than most organizations can assess, making it difficult to separate market momentum from…

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Full Report

Artificial intelligence (AI) is reshaping enterprise software, services and operating models at an unprecedented pace – but most organizations still…

As SG&A Pressure Mounts, a 75% AI Performance Gap Is Emerging

Finance has the clearest view of the artificial intelligence (AI) opportunity. AI World Class research shows organizations redesigning work around…

The Process Mining Value Gap

Process mining provides unprecedented visibility into how work gets done. But many organizations now face a new challenge: hundreds of…