Finance Key Issues: What’s Top of Mind for Executives in 2023

To thrive amid uncertainty, technology and digital transformation will be key.

The prospect of a global economic downturn, geopolitical uncertainty and talent shortages driven by long-term demographic shifts all weighed on the minds of executives as they responded to our 2023 Key Issues Study.

Executives are looking to technology as they consider how to manage the forces of change: 45% of executives said they are accelerating digital transformation (automation, advanced analytics and modeling) – more than any other response measured, including capital spending and cost reduction programs. The cloud has moved to the forefront as the platform organizations must leverage for agility, growth and transformation. In the study, 42% of enterprises reported having legacy solutions that must be replaced.

But organizational disconnects hold back many companies from achieving the transformation they are targeting. More than one-quarter of study participants across business functions said the inability to successfully transform their business and related functions is of key concern.

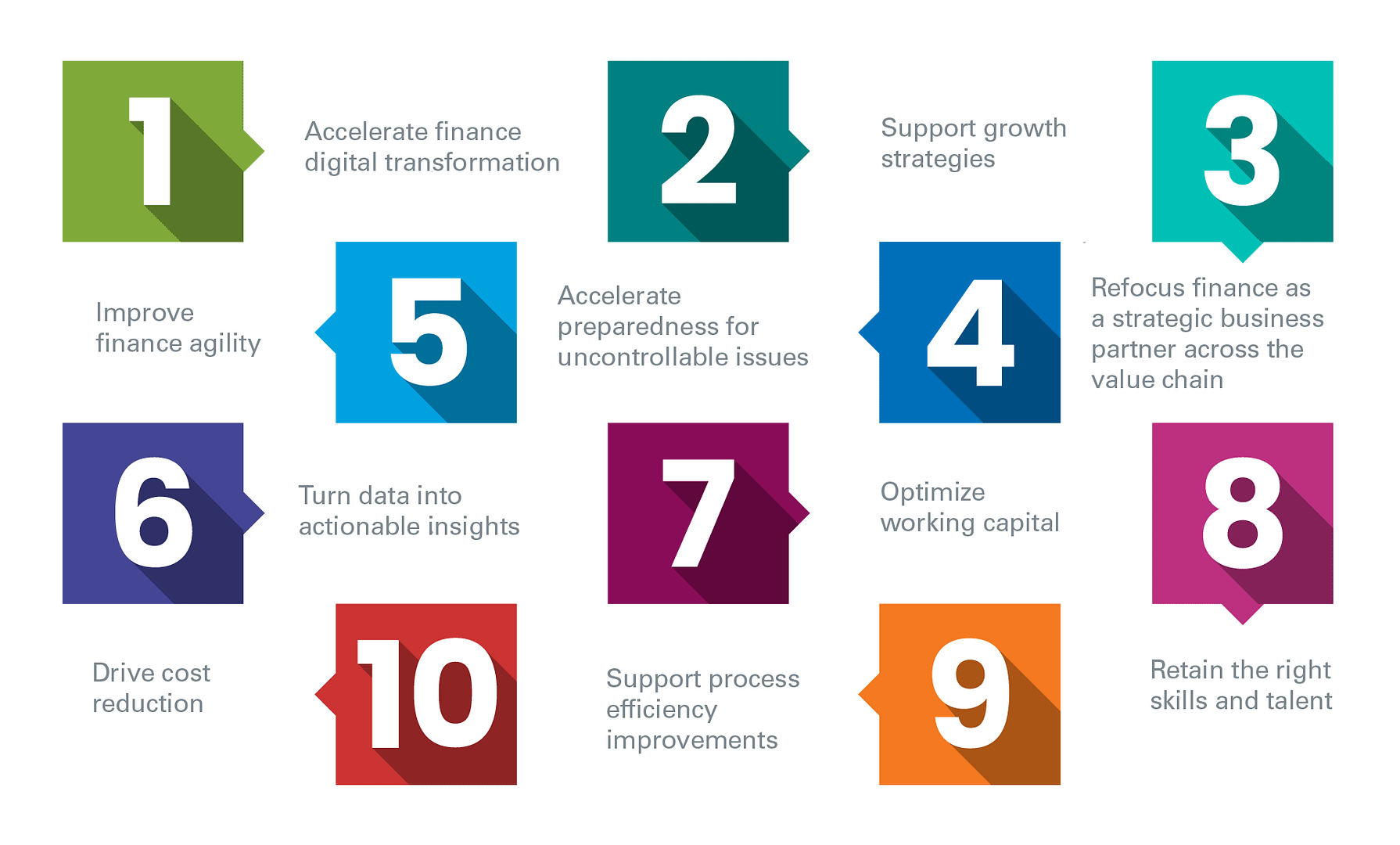

Amid unprecedented uncertainty, finance executives ranked their priorities for the coming year

With the winds of change, finance priorities are shifting

Accelerating digital transformation remains the top finance priority for 2023. Business partnering, finance agility and turning data into insight remain among the top six priorities for 2023 – but the study did observe some shifts, notably accelerated emphasis on preparedness for uncertainty. Additionally, the fact that supporting growth strategies is in the top 10 for the first time in three years is a sign of optimism.

On the other hand, cost reduction moved down the priority list by four spots from No. 6 in 2022, as companies have navigated the pandemic and extracted savings. But make no mistake: Organizations will continue to focus on efficiency. Through our analysis of Digital World Class® finance organizations, we know that these performance leaders have a $39 million cost advantage.

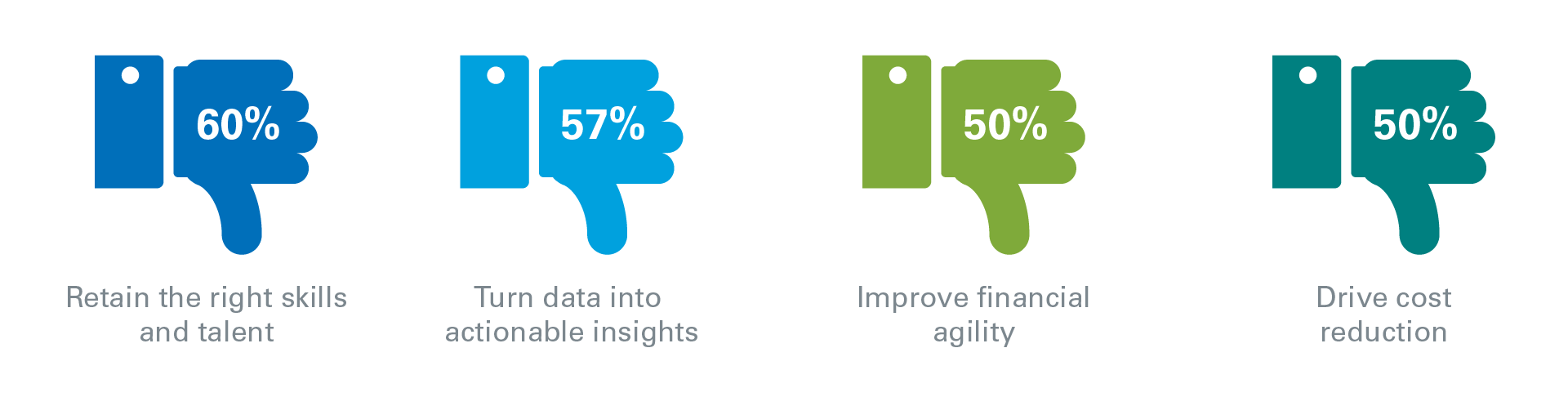

Chief financial officers (CFOs) are concerned about their ability to achieve some key priorities

At least one-half of executives surveyed expressed a low degree of confidence in their current ability to address several of the top priorities.

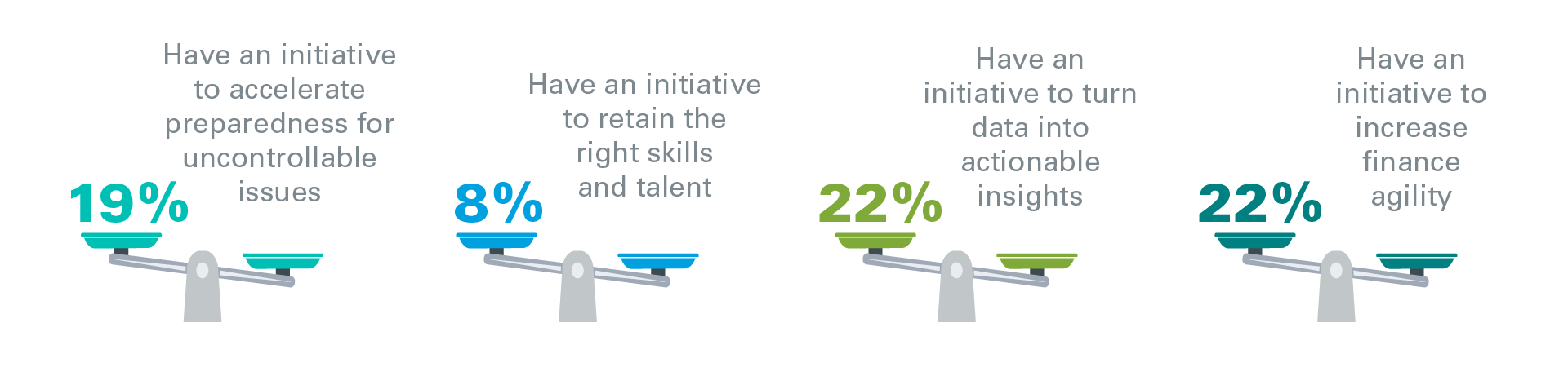

There are significant disconnects between finance priorities and planned initiatives

Not surprisingly, 73% of finance organizations have a major initiative to support digital transformation. What is revealing is that fewer than one-third of organizations have a major enterprise initiative aligned with any of the other nine top priorities.

For example, while retaining the right skills and talent is a top 10 objective, only 8% of finance organizations have a major 2023 initiative planned to address this. This is particularly notable given that only 40% of finance executives expressed high confidence in their ability to meet this objective in 2023 –lowest among the 2023 top 10 objectives. Additionally, talent issues rank among the top hurdles to implementing finance transformation in 2023. Failing to address skills and talent now can have long-term implications.

Significant and meaningful progress won’t happen without action. Therefore, finance executives need to do a better job of properly aligning resources and priorities.

Once again, finance executives must find ways to do more with less

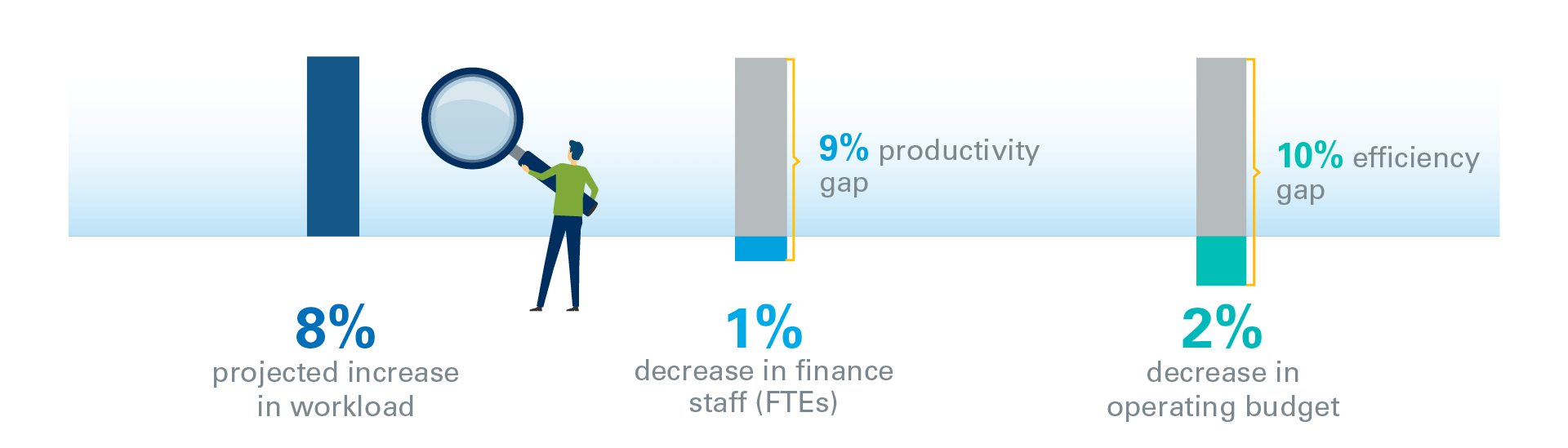

Addressing these diverse priorities will require resources and transformational expertise. The Key Issues Study confirms and quantifies what finance executives already know: They must find a way to do more with less. In 2023, the finance workload is predicted to increase by 8%, but head count and operating budget will drop slightly. This creates a productivity gap of 9% and an efficiency gap of 10%. These gaps have grown significantly from last year’s study – when the gaps were 5.3% and 5.4%, respectively. Finance executives must be prepared to address them head on.

Staffing shortages and the challenges associated with retaining the right skills and talent are forcing finance organizations to look beyond direct staffing. As a result, they are evaluating various geographies and centers of excellence, and increasing reliance on external resources to ensure work gets done. In particular, finance executives project a 53% increase in work volume moving to low-cost locations and/or outsourcing arrangements in 2023.

Finance leaders will rely on technology and digital transformation to close the gaps

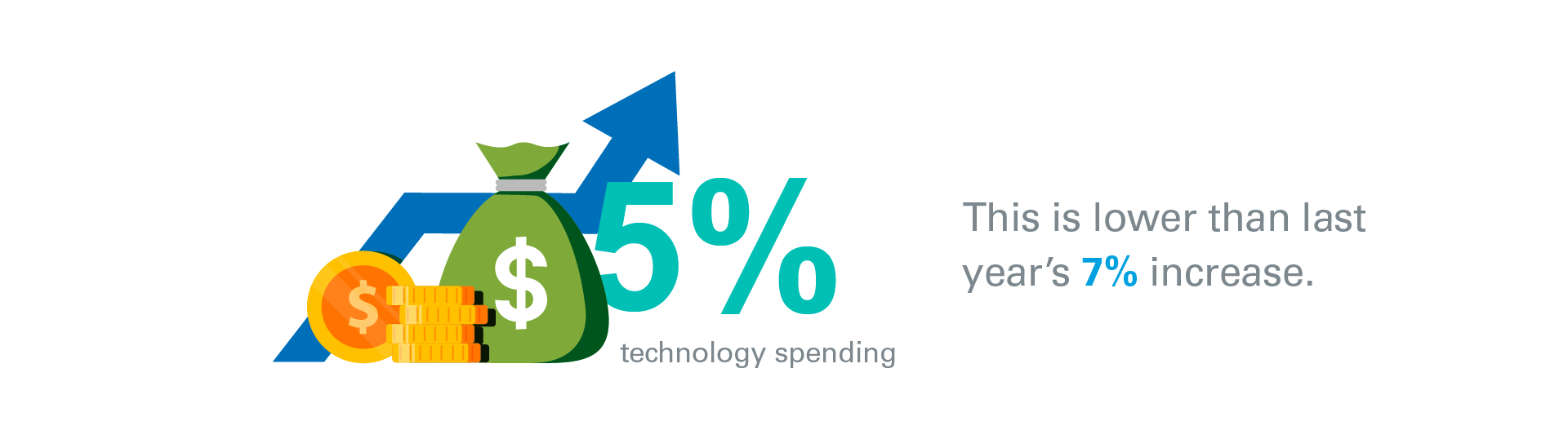

Overall, finance leaders expect a 5% increase in technology spending, indicating a growing reliance on technology to increase productivity, efficiency and effectiveness.

While positive, this is actually a reverse of last year’s study findings, where the projected increase in technology spending (7%) exceeded the projected increase in finance workload (4%). The fact that projected workload will grow faster than technology spending in 2023 implies that companies will need to consider means other than just technology to increase productivity.

Where finance is investing

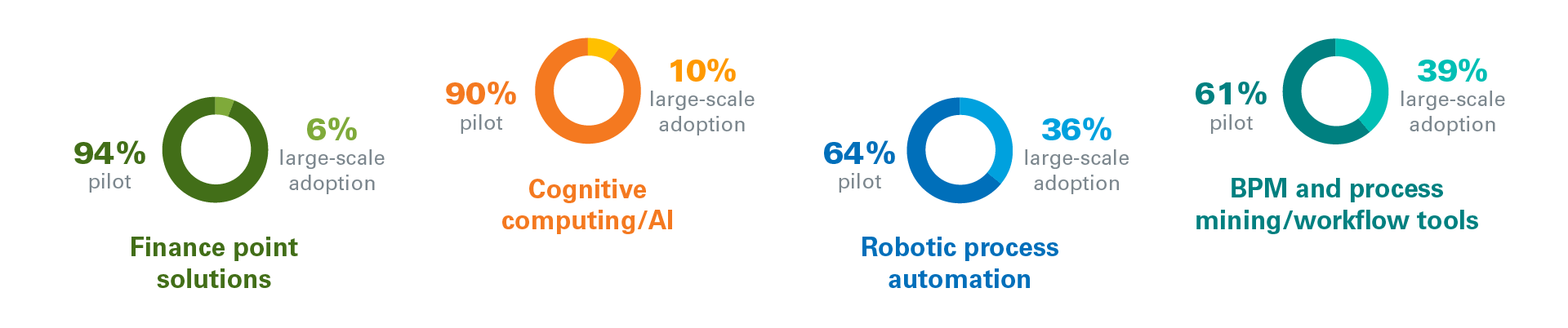

Finance leaders must be prepared to invest in technology to reduce cost and create new capabilities through aggressive adoption of the cloud, robotic process automation (RPA), analytics, and other tools. The Key Issues Study looked at current adoption levels of digital technologies, as well as projected increases in adoption in 2023. Executives expect the greatest growth in adoption for RPA (19%), business process management (BPM) and process mining/workflow tools (19%), and core finance application suites (17%).

Many finance technologies largely meet or exceed expectations today:

Despite delivering on business goals, many digital technologies remain stuck in the pilot phase

For finance to succeed, digital technologies need to achieve enterprise scale. Currently, they do not. This means finance organizations have significant opportunities to expand these beyond pilot projects or small-scale deployments.

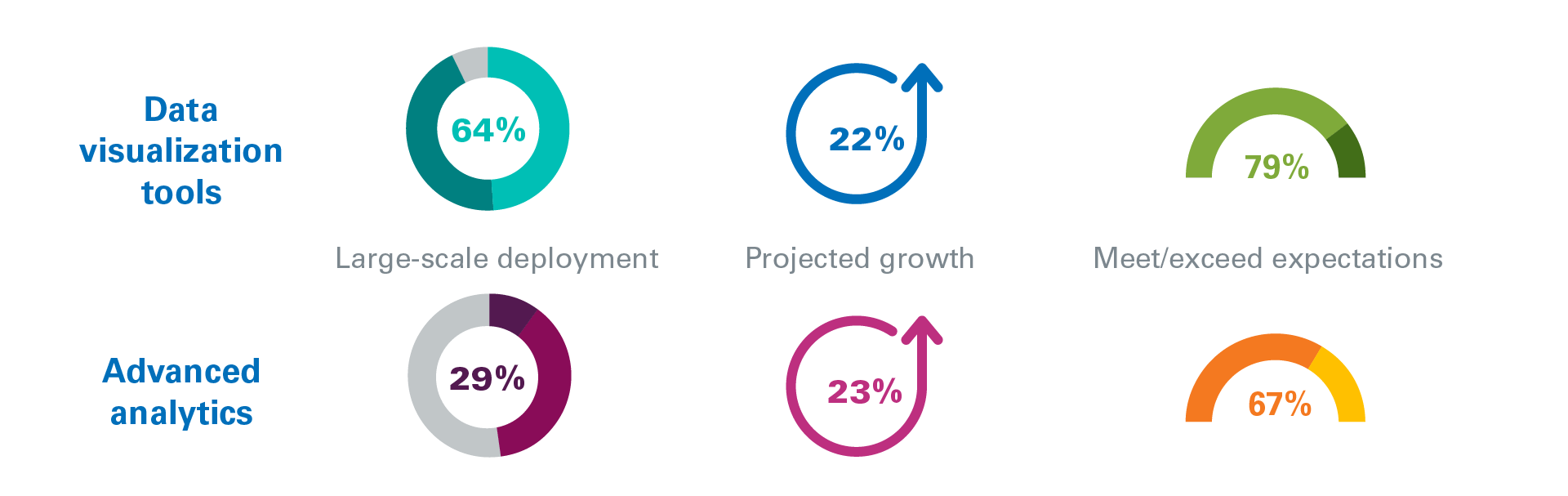

Analytics adoption also remains mixed

Finance must secure data and harness it into meaningful and actionable business insight that is complete and timely. Here again, finance leaders should focus on elevating these initiatives past the pilot stage or small deployments, particularly given that data-related technologies meet or exceed business objectives most of the time. This is particularly true for advanced analytics.

Master data management initiatives have a higher tendency to miss their objectives, likely due to the complexities of mastering data quality.

Currently, only 22% of finance organizations have a 2023 initiative to turn data into actionable insight. Those that are taking action are increasing access to self-service and data-discovery tools (74%), upskilling and training staff (67%), and democratizing data and analytics within and beyond finance (59%). Nearly one-half of organizations (48%) have established an analytics/reporting center of excellence (COE).

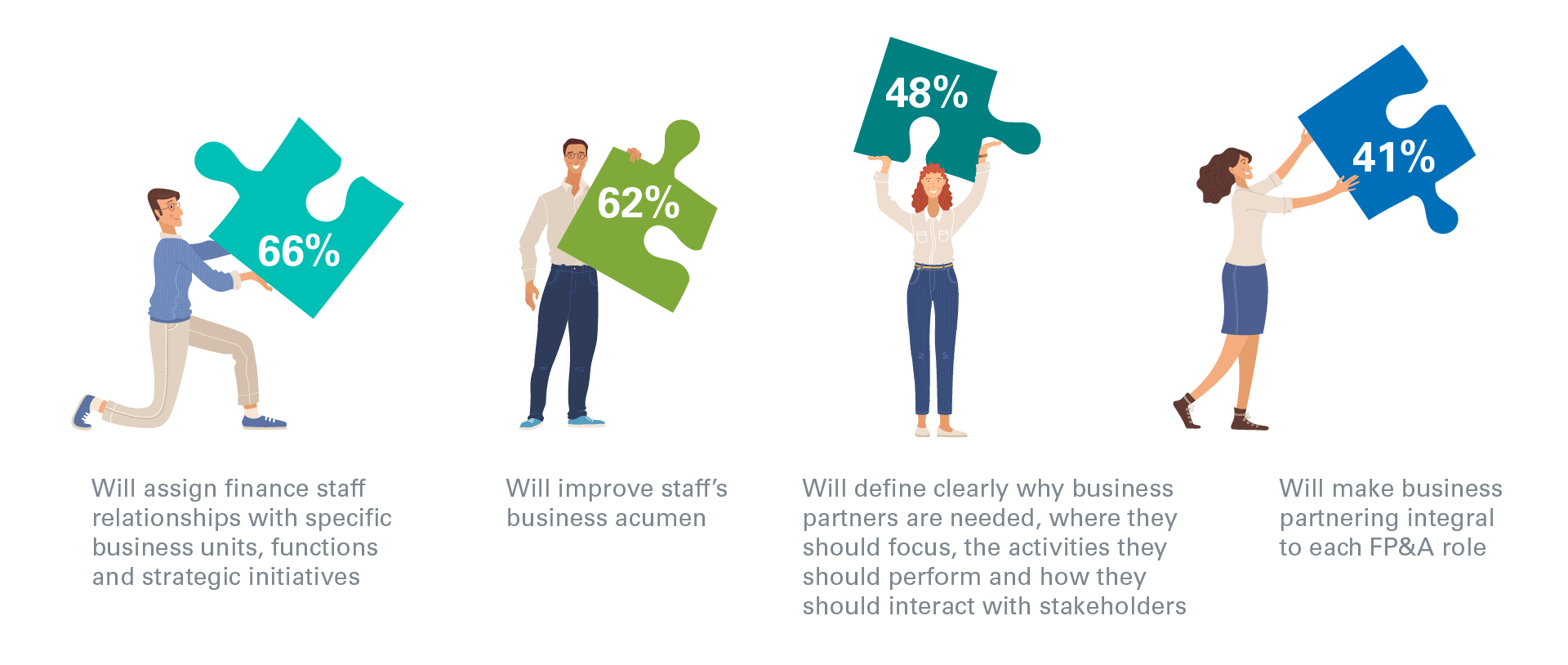

Strategic business partnering is a key part of the transformation puzzle

Finance leaders are emphasizing cross-functional business partnering, business aptitudes and work prioritization as the top ways to become a strategic business partner. Of concern, though, nearly one-quarter (21%) of finance organizations are not actively planning or executing on business partnering initiatives.

Be ready to navigate the roadblocks

Study participants ranked their top 10 hurdles impeding finance transformation in 2023:

- Inadequate funding and resource allocation

- Skills deficiencies and/or capacity constraints of the organization

- Process complexity

- Organizational complexity

- Organizational resistance to change

- Overcommitment

- Lack of a comprehensive finance transformation strategy and roadmap

- Lack or deficiency of critical skills

- Lack of management systems and related incentives for transforming

- Data-related issues

Resources, skills, complexity and resistance are perennial hurdles to finance transformation. But several roadblocks on this list stood out: lack of a comprehensive finance transformation strategy and roadmap, and lack of management systems and related initiatives. Both of these are well within finance executives’ control – if their resources and priorities are well aligned.

Sharpen your focus for 2023

We believe finance executives must look beyond the typical recession playbook when honing their plans. Certainly, realigning investments to reflect current top priorities is critical for making meaningful progress toward objectives. Here’s what else we think will make the biggest impact in 2023:

- Bring digital technologies to scale to fast-track transformation through process automation, advanced analytics and cloud migration.

- Partner with human resources to upskill and reskill your people with high-demand digital capabilities.

- Accelerate application, data and platform migrations that enable use of analytics at scale, while also increasing your ability to deliver timely business insight.

- Push toward a future operating model that leverages COEs, customer-facing business units, global business services and strategic partnerships in new ways to enhance agility.

Featured Insights

SG&A Has Reached a Tipping Point

Selling, general and administrative (SG&A) costs have reached a five-year high across Europe’s largest companies. Even with stronger revenue growth,…

Revenue Is Growing. SG&A Costs Are Growing Faster.

SG&A costs have outpaced revenue growth for five consecutive years at North America’s largest companies. Even organizations improving selling, general…

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Summary Report

Artificial intelligence (AI) capabilities are advancing faster than most organizations can assess, making it difficult to separate market momentum from…

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Full Report

Artificial intelligence (AI) is reshaping enterprise software, services and operating models at an unprecedented pace – but most organizations still…