How US Companies Plan to Spend Their 2017 Tax Reform Windfall

The 2017 tax reform was intended to incentivize US companies to repatriate overseas’ cash and use their tax savings to increase domestic investment. This is not the first time Congress has authorized a repatriation tax holiday. It gave companies an even more generous break in 2004, as part of the American Job Creation Act. At the time, companies repatriated anywhere between $350 to $500 billion, depending on who you ask.

But things didn’t turn out too well. Market experts estimate that as much as 91 cents on the dollar went toward share buybacks and dividends. At the same time, US companies were hemorrhaging jobs.

Are things turning out differently this time?

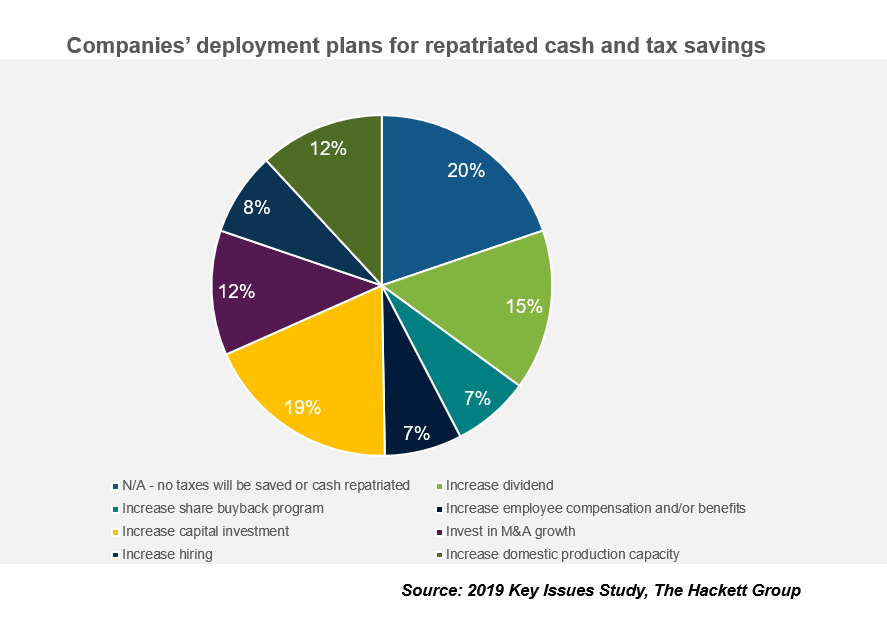

The Hackett Group’s 2019 Key Issues Study shows that nearly half of the companies in our study said that the additional funds will be spent on increasing domestic production, capital investment, hiring, and higher employee compensation. Only 22% listed dividends and buybacks (see chart below).

These numbers look a lot more promising. Yet they don’t jive with the study’s other findings. Finance executives identified cost reduction as their number-one initiative for the year. Case in point: On January 11, GM reported 2018 earnings, at above analysts’ expectations, and it predicted 2019 earnings will be even higher. But it attributed growth to shutting down plants and laying off workers. Economic headwinds and volatile markets are driving companies and finance organizations to emphasize cost optimization this year. Our study also revealed finance’s headcount is expected to shrink as is its operating budget.

In addition, during 2018, record low interest rates led to record high corporate borrowing. CNBC reported recently that the past year’s cash-to-debt ratio was the worse since 2008. Enough said. The debt burden is particularly striking for organizations on the precipice of falling below investment-grade ratings. It would make sense for them to reduce cost by paying down debt.

How then to reconcile the two sets of data?

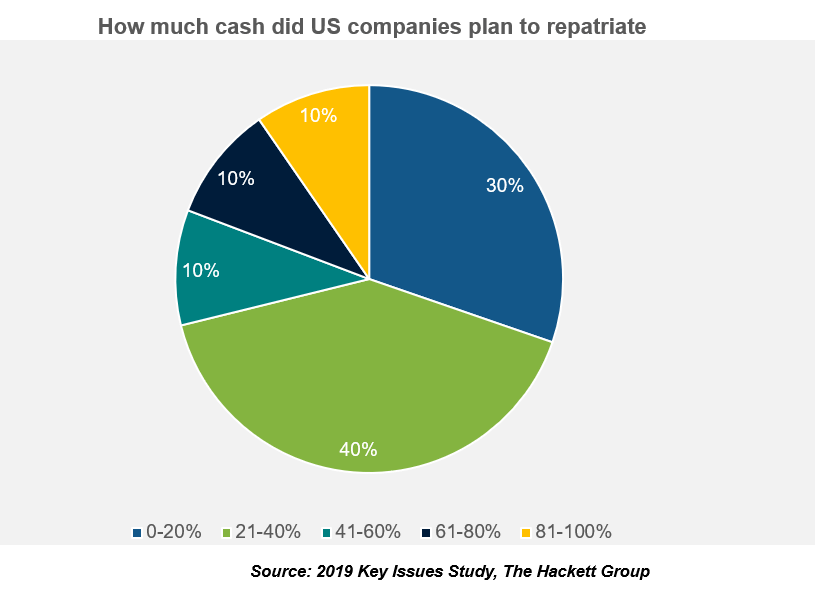

One explanation is that 20% of US companies in our study said that they did not realized any tax benefits. Another is that while the allocation appears a lot closer to the spirit of the law than in 2004, the sum of repatriated cash may be a lot smaller. The chart below indicates that 70% of US companies had plans to repatriate less than 40% of their overall offshore cash. That may be because they tagged that cash for expansion overseas. The tariff war would certainly be a factor in that decision. Plus, the tax holiday this time (15%) was less generous than in 2004)

Finance plays a critical role in driving capital allocation decisions. It provides the analyses of current and projected performance that support management choices. In our work with clients, we have noticed that decisions on how to spend capital are often based on different models within the same company or gut-feel vs. data-driven models. It’s going to be finance’s job this year to make sure the organization deploy consistent and unbiased methodologies to make critical investment decisions.

Related Insights

SG&A Has Reached a Tipping Point

Selling, general and administrative (SG&A) costs have reached a five-year high across Europe’s largest companies. Even with stronger revenue growth,…

Revenue Is Growing. SG&A Costs Are Growing Faster.

SG&A costs have outpaced revenue growth for five consecutive years at North America’s largest companies. Even organizations improving selling, general…

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Summary Report

Artificial intelligence (AI) capabilities are advancing faster than most organizations can assess, making it difficult to separate market momentum from…

AI Solution Providers: 2026 Trends, Capabilities and Strategic Insights – Full Report

Artificial intelligence (AI) is reshaping enterprise software, services and operating models at an unprecedented pace – but most organizations still…