Quantifying the Finance Digital Opportunity

We’re finance people. And finance people like numbers. For many, a current pressing question is how to measure the dollars and cents benefits of digital transformation. There are a lot of “savings estimates” floating around, but most come from vendors. And finance professionals are rightfully skeptical. So, at The Hackett Group, we took on the challenge of putting numbers to the digital advantage, leveraging our database of 100s of companies and 1000s of finance benchmarks.

We focused on assessing the impact of digitization on finance efficiency first. That’s because cost is a huge issue for companies right now. Senior executives are wary of signs of a global economic slowdown, escalating trade wars and intensified competition driven by disruptive technologies. Cost optimization is finance’s number-one improvement priority for the year, according to The Hackett Group’s 2019 Key Issues Study.

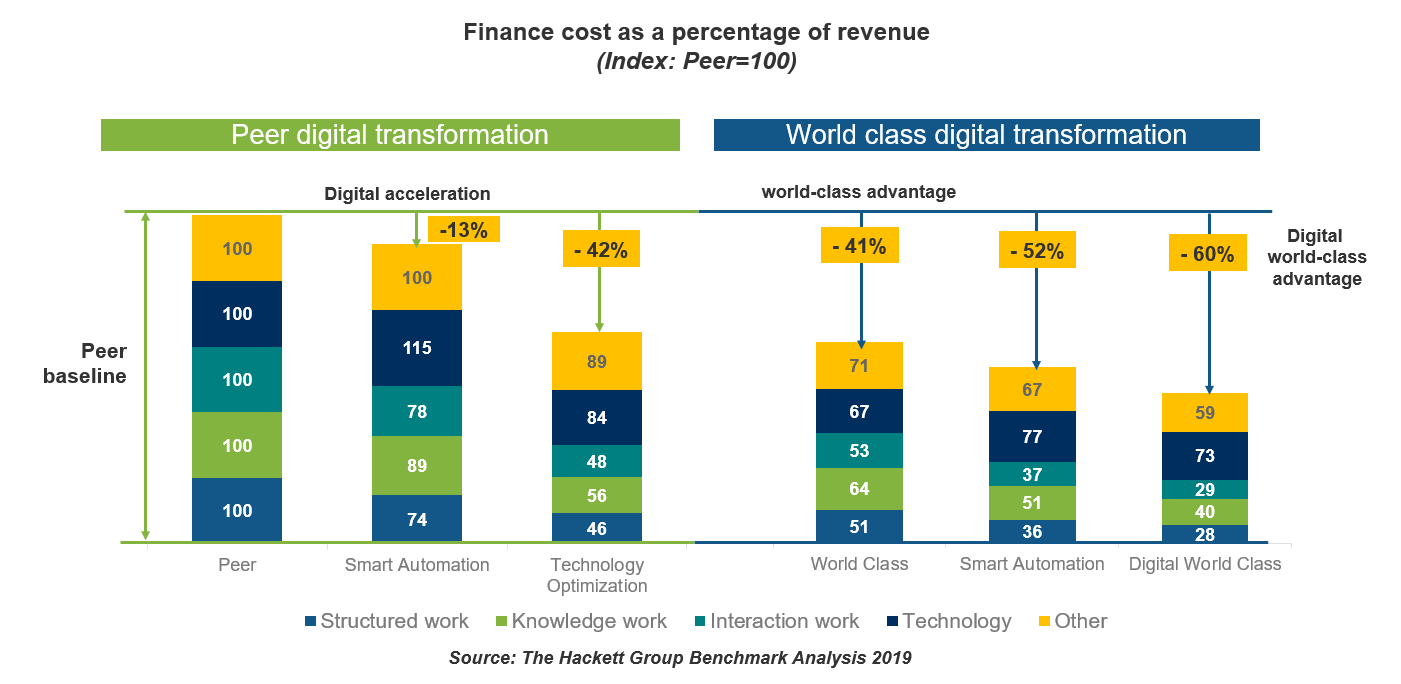

We ran out data through a model designed to assess digital maturity. We found that going all-out digital can have an enormous impact on finance cost, for both typical and what we label world-class finance organizations. It can catapult typical finance functions to today’s world-class status.

Going from the left all the way to right on the chart above, however, will take a lot of time and resources. So, waiting is not an option. Our analysis shows that finance can get an immediate boost from adopting smart automation technologies, like RPA and cognitive, which are faster to adopt and produce a quicker ROI. We call this the digital “accelerator.” Quick hits won’t get you to the finish line, but they will get you there sooner.

What’s Smart Automation?

At The Hackett Group, we define smart automation as a category of technologies used to optimize structured, knowledge and interaction work through the deployment of RPA, smart data capture, conversational interfaces, cognitive computing and agile orchestration technologies. What makes these technologies “smart?”

- They’re agile and easily adaptable to changes in business demand

- They’re faster and more economical to develop, implement and maintain

- They’re modular, enabling organizations to start small with any particular element and then integrate others to add functionality and scale

- They’re flexible enough to address multiple problem sets across most processes (i.e., it is not function or process specific)

- Finally, they are business-owned, led and driven with close collaboration and support from information technology (IT) – rather than owned and managed by IT – requiring low code or no code

Smart automation allows finance to spend less time on “business as usual” and more time on value-creating activities. So, it can help finance transcend its current “top level maturity level” as a valued business partner to become a catalyst of enterprise change.

Of course, digital leadership is not the only factor that will determine whether finance organization achieve new levels of excellence. (And that bar is rising.) To get to the top, they’ll have to activate other enabling capabilities such as re-skilling talent, changing their service delivery model, improving their analytics capability and starting to think more in terms of customer-centricity. But as we saw in the chart above, technological advances alone can make a huge difference.

In a recent paper by Erik Dorr and Vin Kumar, we offer a roadmap for how finance can realize the full benefits of smart automation: https://www.thehackettgroup.com/smart-automation-fin-1905/

Related Insights

As SG&A Pressure Mounts, a 75% AI Performance Gap Is Emerging

Finance has the clearest view of the artificial intelligence (AI) opportunity. AI World Class research shows organizations redesigning work around…

The Process Mining Value Gap

Process mining provides unprecedented visibility into how work gets done. But many organizations now face a new challenge: hundreds of…

Benchmarking in the AI Age: What Matters Now

How is benchmarking evolving in the AI era, and how are leading organizations using it to set sharper targets, prioritize…

NASDAQ Opening Bell

November 15, 2024 – In honor of the LeewayHertz acquisition, Ted Fernandez, Chairman and CEO of The Hackett Group®, rings…